Your financial net worth is the sum of all your assets, less the sum of all your liabilities. Essentially, this number is the result of building your personal balance sheet. But does a higher net worth mean you’re more likely to meet your financial goals? Let’s consider what your net worth does—and doesn’t—say about you.

You often read financial pundits or hear from financial advisors who recommend tracking your net worth regularly. In fact, updating your balance sheet is one of the steps we recommend for your annual financial housekeeping. However, all in all, your net worth doesn’t tell you all that much about how well you’re doing.

The Value of Net Worth

The value of knowing your financial net worth is in the analysis of your balance sheet.

Take a look at your net worth now versus the last time you calculated it. Is it higher or lower? If it is higher, what caused the change? Was it primarily due to an increase in assets, a decrease in liabilities, or a balance of both? On the other hand, if your net worth has decreased, is it because the value of your assets decreased, your liabilities increased, or both?

Considerations

Here is something else to consider: How much of the change was due to your own activities? For example, did your assets increase primarily because the value of your house increased? Was the increase in value due to work you did on the house, or was it simply due to market forces?

Now consider this: if you’re not planning on selling your house in the very near future, how will the increase in the estimated market value of your home affect your daily life now? The increase in the market value is different than the increased enjoyment or use that you get from the house. Your net worth will reflect the increase in market value of the house but likely won’t reflect the additional enjoyment you experience. Keep in mind that you may make changes to your home that cost money and give you great joy – but that doesn’t always mean that the market value of your house goes up. Beauty is in the eye of the beholder. In that case, on paper, your net worth decreased.

Expenses aren’t reflected

Here’s something else to consider: What happens the next time your town assesses real estate for taxes? If the market value of your home has gone up, your property taxes may go up. In this case, that increase in asset value comes along with an increase in expenses—but expenses aren’t reflected on the balance sheet or net worth. And remember, you don’t benefit from the increased market value of the home unless you sell it.

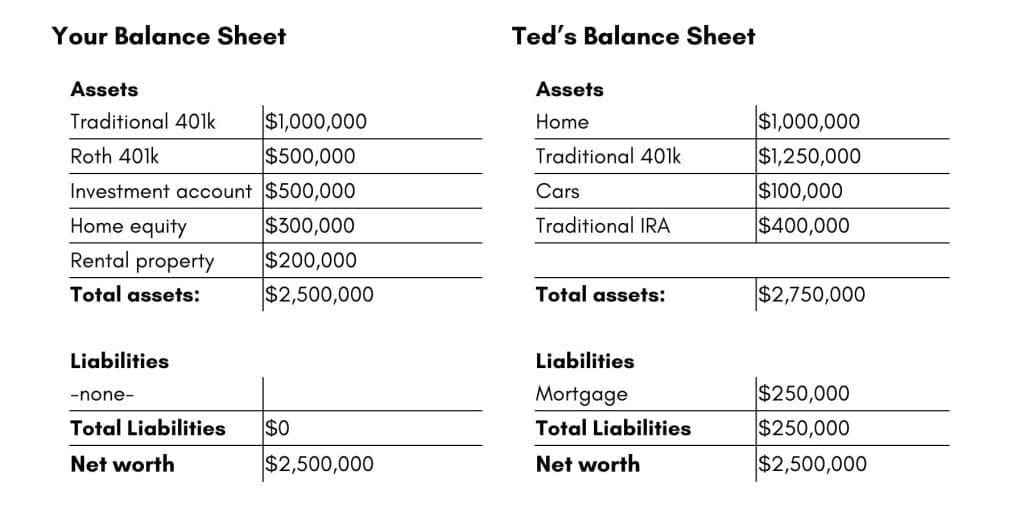

Here’s another consideration – let’s say that you and your twin brother, Ted, each have a financial net worth of $2,500,000, and you’re 60 years old and ready to retire. Your balance sheets are below.

Both balance sheets show a net worth of $2,500,000. They do show the difference in assets and liabilities. And in this case, we labeled the types of accounts. What you don’t see is the mortgage payment that Ted will be making or the rental income you’ll be receiving from your rental property. They also don’t show the impact of taxes as you use your assets. Withdrawals from a traditional 401k and a traditional IRA will be fully taxable (assuming that contributions were pre-tax). Withdrawals from a Roth 401k account won’t be subject to income tax. The amount of money available for spending each month after taxes will be very different if you withdraw from a traditional 401k or IRA as opposed to a withdrawal from a Roth 401k.

Is there any benefit to tracking net worth?

There is some value in periodically updating your balance sheet and determining your net worth. The process alone makes you re-visit your assets and liabilities and perhaps consider how well they work for you. And, if your primary focus at this point is paying down debt, seeing the increase in net worth can be motivating. However, beyond that, your net worth is what you can expect to end up with if you sell everything at fire sale prices and pay off all debt with the proceeds. Generally, the only time you do that is upon death or if you’re moving to a desert island and starting over. You could have a net worth of millions of dollars and still be unable to live the life you want – even a modest lifestyle – if you can’t use your assets. If your assets don’t generate income and can’t be used to cover expenses, they aren’t helping you live your life today.

Other tools are often more helpful in measuring your progress towards the life you want. Few people we’ve worked with have a financial goal of accumulating a specific dollar amount in an account. Perhaps, if they’re saving for a down payment or some other large outflow, they may have a specific amount they want to accumulate. But even then, that would be only one aspect of their financial lives.

More often, a financial goal is the ability to DO something. That something may be to travel, reduce working hours, pay for college, or even retire. But as we mentioned, there’s more to pursuing and meeting a goal than accumulating a specific account balance. The same net worth in the above example does not mean the same ability to generate income or cover living expenses. Where your money comes from and where it goes, and ensuring you’re using your financial resources efficiently is critical to meeting your goals. Those factors are not considered in a balance sheet, and they aren’t reflected in your net worth.

Other financial tools

Even if your goal is to pay off a loan, much of that will depend on cash flow – not assets. The result of paying off the loan will be evident on your balance sheet. But the process won’t be.

Try including other tools rather than focusing solely on your balance sheet and net worth to measure your progress. A cash flow statement shows where your money comes from and where it goes. You’ll be able to see what percentage of your income goes to each of your categories of expenses. Then, you can determine if your spending is actually aligned with what’s important to you. And, something that is often overlooked, you can consider the impacts of changing your income as well. Growing your income, perhaps by starting a side gig, changing jobs, or investing to generate passive income, will affect your cash flow and possibly your ability to meet your goals. Think of your balance sheet as showing what you have and your cash flow statement as showing what you can do.

Beyond a cash flow statement that reflects your current income and outflows, you may want to do some projections, also called a pro forma cash flow statement. For instance, consider inflation for your projected expenses or the result of a salary increase due to a job change. Or, simply project the impact of a change in spending or savings habits.

The big picture

In most cases, you’ll want to use a combination of balance sheet information and cash flow information to make financial decisions. Your balance sheet may give you an idea of what you have available to start a business. But you’ll need cash flow projections to determine the financial impact on your life over time. The balance in a bank account may help you determine how much you can put down on a real estate purchase – but the cash flow statement will let you see whether you can afford ongoing debt payments, taxes, utilities, etc.

Ultimately, what your net worth says about you is where you are right now. It doesn’t say where you’ve been or what you can accomplish. It doesn’t even say that you are or you aren’t meeting your goals. However, the process of calculating your net worth and thinking about how it changes over time can be enlightening.

This article is intended to be educational and thought-provoking rather than financial advice. When we work together in a financial planning engagement, we discuss your unique personal situation and your unique goals. We examine these factors and many others during our financial planning process to determine appropriate financial strategies for YOU.